AI Agents in Insurance Operations: Why Manual Workflows Are a Liability

Manual workflows in insurance are not just slow — they are becoming a structural competitive disadvantage. AI agents are already executing multi-step operations across claims, underwriting, and customer service at carriers that have chosen to move. The insurers still relying on human-first, document-heavy processes are not being patient. They are falling behind.

At Tenfold, we work with operations leaders who are done running pilots and ready to deploy. This post is for them — and for anyone still weighing whether the shift to agentic AI in insurance is real, urgent, or worth the organizational lift.

Quick Answer: AI agents in insurance operations are autonomous systems that execute end-to-end workflows — from claims intake to underwriting decisions to policy updates — with minimal human intervention. They are live in production at leading carriers today, and the operational gap between adopters and laggards is widening fast.

Key Takeaways:

Agentic AI is already in production across claims, underwriting, and back-office insurance functions — this is not a pilot-stage technology.

Insurance carriers using AI automation are reporting 30–50% reductions in processing costs compared to manual workflows.

AI has compressed standard underwriting decision time from multiple days to under 13 minutes while maintaining accuracy above 99%.

82% of carriers are planning agentic AI adoption within three years — the window to lead is narrowing.

The bottleneck is not AI capability. It is that most insurance orgs are not yet structured to delegate workflows to it.

What "AI Agents" Actually Means in an Insurance Context

AI agents are not chatbots. They are not search tools. According to Deloitte, AI agents are "autonomous systems designed to analyze data, identify patterns, and execute tasks with minimal or no human intervention" — and unlike static AI models, they actively engage in problem-solving, decision-making, and automating complex workflows without requiring user input.

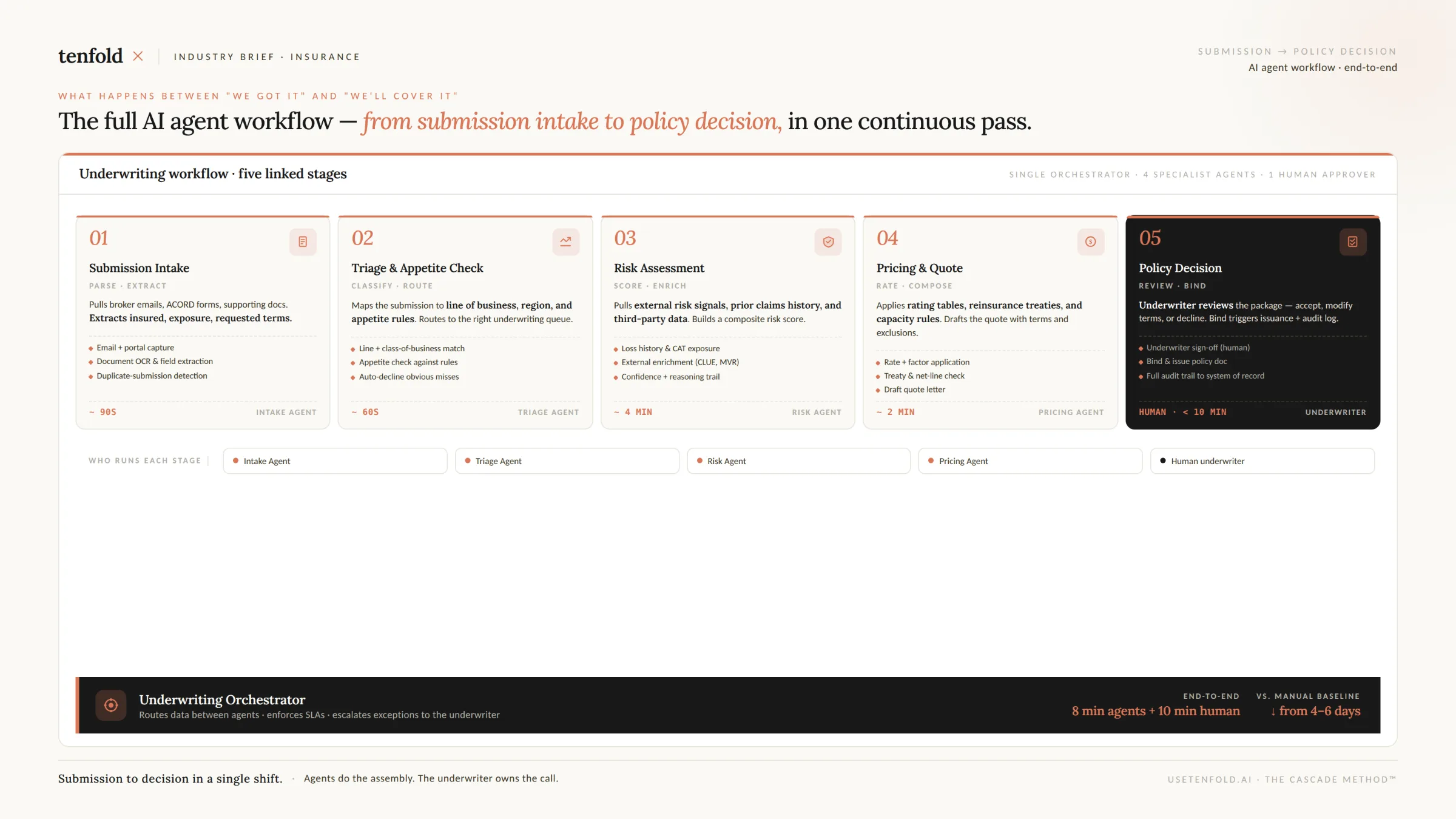

In insurance, this distinction matters enormously. A chatbot answers a question. An AI agent receives a new commercial submission, normalizes data from multiple sources, identifies missing exposure information, reaches out to the broker to resolve gaps, and routes a decision-ready risk to the underwriter — all without a human touching the file.

McKinsey describes this architecture clearly: agentic AI in insurance combines autonomous workflow chaining, multi-agent collaboration between specialized modules, and contextual memory that maintains persistent policyholder profiles across touchpoints. The result is end-to-end processing of commercial policies with little or no human intervention.

Where Manual Workflows Are Breaking Down First

Three operational areas are absorbing the most agent-driven displacement right now:

Claims Processing

Claims represent the highest-cost function in insurance. According to Databricks, claims processing accounts for 70% of a property insurer's expenses — making it the most consequential target for automation. Traditional workflows — physical damage inspections, manual document review, fraud analysis, payment calculation — are being systematically replaced.

Insurance carriers using AI automation are reporting 30–50% reductions in processing costs for AI-automated workflows compared to manual processes. UK insurer Aviva deployed more than 80 AI models across its claims domain, cutting liability assessment time for complex cases by 23 days, improving routing accuracy by 30%, and reducing customer complaints by 65%. These are not lab results — they are live operational numbers.

Agentic AI systems review documents, verify coverage, communicate with policyholders, and flag anomalies autonomously. Human adjusters step in only when something requires genuine judgment. Analysts project that by late 2026, more than 35% of insurers will deploy AI agents across at least three core functions, cutting processing time by up to 70%.

Underwriting

Underwriting has historically been a document-intensive, analyst-heavy function. AI is compressing that timeline aggressively. According to a 2025 technical analysis cited by BizTech Magazine, AI has reduced the average underwriting decision time from three to five days down to 12.4 minutes for standard policies, while maintaining a 99.3% accuracy rate in risk assessment.

Allianz UK's implementation of its BRIAN AI tool is a precise example of agentic AI in underwriting. The tool saved approximately 135 working days in information gathering in the period following its January 2025 rollout — replacing hours of manual search through 600-page guidance documents with instant, structured answers.

For complex commercial lines, Deloitte documents a Submission Interpreter Agent that standardizes and normalizes data from multiple sources so underwriters receive clean, structured information — without manual intervention. A parallel Optimal Coverage Recommendation Agent identifies missing information and resolves exposure gaps before the underwriting process even begins.

77% of insurers have already integrated AI into their underwriting workflows according to master.of.code data cited by AlchemyCrew Ventures. This is not a trend to track. It is a baseline to meet.

Back-Office and Customer Operations

Fraud detection, policy issuance, billing, and customer service are the third surface area where manual workflows are being displaced. AI agents can identify patterns and anomalies in claims data to flag fraud — with leading fraud detection AI achieving 90%+ accuracy according to AlchemyCrew Ventures. Health insurers are using AI across prior authorizations, risk adjustment, plan design, and claims adjudication, according to NAIC survey data.

On the customer-facing side, virtual agents handle policy queries, claims status updates, and even initiate claims — 24 hours a day. When a customer contacts a carrier, an AI agent can identify intent, route the interaction to the correct workflow, trigger post-call actions like CRM updates and document dispatch, and flag at-risk policyholders for retention teams — all in a single interaction.

The Real Barrier: It Is Not the Technology

The Insurtech market is growing at a 36% CAGR through 2034. 82% of carriers are planning agentic AI adoption within three years. The technology is proven, the use cases are documented, and the ROI is measurable.

So why are so many insurance operations still running on manual workflows?

The answer is organizational, not technical. Most insurers have not redesigned their processes around delegation to AI agents. They have bolted automation onto existing workflows rather than rebuilding workflows to be agent-first. The result is marginal efficiency gains where transformational ones are possible.

At Tenfold, we have seen this pattern across industries — and the fix is not a longer pilot. It is a different operating model: one where AI agents own the routine, humans own the exceptions, and the entire workflow is designed from the ground up for that division of labor.

The firms pulling ahead are not deploying more software. They are deploying a different way of working.

Summary

AI agents in insurance operations are not approaching — they are already displacing manual workflows in claims, underwriting, fraud detection, and customer service at carriers that have made the structural decision to move. The data is unambiguous: faster cycle times, lower processing costs, and materially better accuracy. The gap between carriers deploying agentic AI and those still running manual-first operations is compounding. Tenfold works with operations leaders who are ready to close that gap — not with a proof of concept, but with a production-ready implementation model.

Frequently Asked Questions

Q: What is an AI agent in insurance, and how is it different from RPA or a chatbot?

A: An AI agent is an autonomous system capable of executing multi-step workflows — analyzing data, making decisions, and taking action — without human input at each step. Unlike RPA, which follows rigid rules, agentic AI understands context and adapts. Unlike a chatbot, it does not just respond — it acts. In insurance, that means an agent can process a claim from intake to payment without a human touching the file for standard cases.

Q: Which insurance functions are most ready for AI agent deployment today?

A: Claims processing, underwriting intake, fraud detection, and customer service operations are the most mature use cases with the most documented ROI. Carriers like Aviva have already deployed AI at scale across claims with measurable results. Underwriting triage and submission normalization are the fastest-growing deployment areas heading into 2026.

Q: What does it take to implement AI agents in insurance operations?

A: Successful implementation requires three things beyond the technology: clean, accessible data infrastructure; redesigned workflows that are built for agent-first execution rather than retrofitted; and governance frameworks that satisfy regulatory auditability requirements. Most insurers that struggle to scale AI are missing at least one of these. A partner with implementation experience — not just a vendor — makes the difference.

Q: How long does it take to see ROI from AI agent deployment in insurance?

A: In documented implementations, meaningful efficiency gains appear within months of production deployment — not years. Aviva's 23-day reduction in liability assessment time and Allianz's 135 working days saved in information gathering both came within the first year of deployment. The ROI timeline depends on use case complexity and readiness of data infrastructure.

Q: Is agentic AI in insurance compliant with current regulations?

A: Regulatory frameworks are evolving alongside adoption. As of late 2025, 23 states and Washington D.C. had adopted the NAIC's AI Model Bulletin, which requires insurers to establish governance, documentation, and audit procedures for AI systems. Compliant deployment is achievable — but it requires choosing systems that are explainable, auditable, and designed for regulatory transparency from the start.